NABE Business Conditions Survey

July 2020

NABE Survey Shows Last Quarter One of the Worst Since Global Financial

Crisis, But Sharp Rebound in the Three-Month Outlook

The July 2020 NABE Business Conditions Survey report presents the responses of 104 NABE members to a survey conducted July 2-14, 2020, on business conditions in their firms or industries, and reflects second-quarter results and the near-term outlook.

COMMENTS: “NABE’s Business Conditions Survey reveals firms are using a number of levers to manage costs and adapt to the economic reality of COVID-19,” said NABE President

Constance Hunter, CBE, chief economist, KPMG. “Respondents are more optimistic about the outlook for the next 12 months than they were in the April survey. In April, most respondents expected the inflation-adjusted gross domestic product to contract from the first quarter of 2020 to the first quarter of 2021; in the current survey, two-thirds of respondents expect an expansion from the second quarter of 2020 to the second quarter of 2021.”

“Respondents in this survey report a significant snapback in expectations from the depths reached across nearly all categories in April, suggesting that the economy and business operating environment are no longer on quicksand after the COVID-19 lockdowns in the United States and elsewhere,” added NABE Business Conditions Survey Chair

Megan Greene, senior fellow, Harvard Kennedy School. “Firms’ outlooks over the next three months improved for sales, profit margins, prices, employment, and capital spending. At the same time, respondents report that last quarter was the worst since the global financial crisis for sales, prices, and capital spending.

“Firms have imposed a number of special measures to limit the negative financial impact of COVID-19 on their firms, including freezing hiring and terminating and furloughing employees,” continued Greene. “One in three firms has resumed normal operations, but nearly as many respondents say they don’t expect their firms to return to normal operations for more than six months. The vast majority of respondents anticipate COVID-19 will lead to more flexible hiring and work arrangements in the future, with 80% reporting their firms will continue to have some degree of remote working for employees post-crisis.”

HIGHLIGHTS

HIGHLIGHTS

• The panel’s consensus outlook for the U.S. economy, measured by year-over-year growth in inflation-adjusted gross domestic product (real GDP), improved considerably in July compared to that in the previous survey. Two-thirds (66%) of panelists expect real GDP to increase from the second quarter (Q2) of 2020 to Q2 2021, including 16% who expect real GDP to increase more than 6%. About 31% of respondents expect flat or declining real GDP over four quarters.

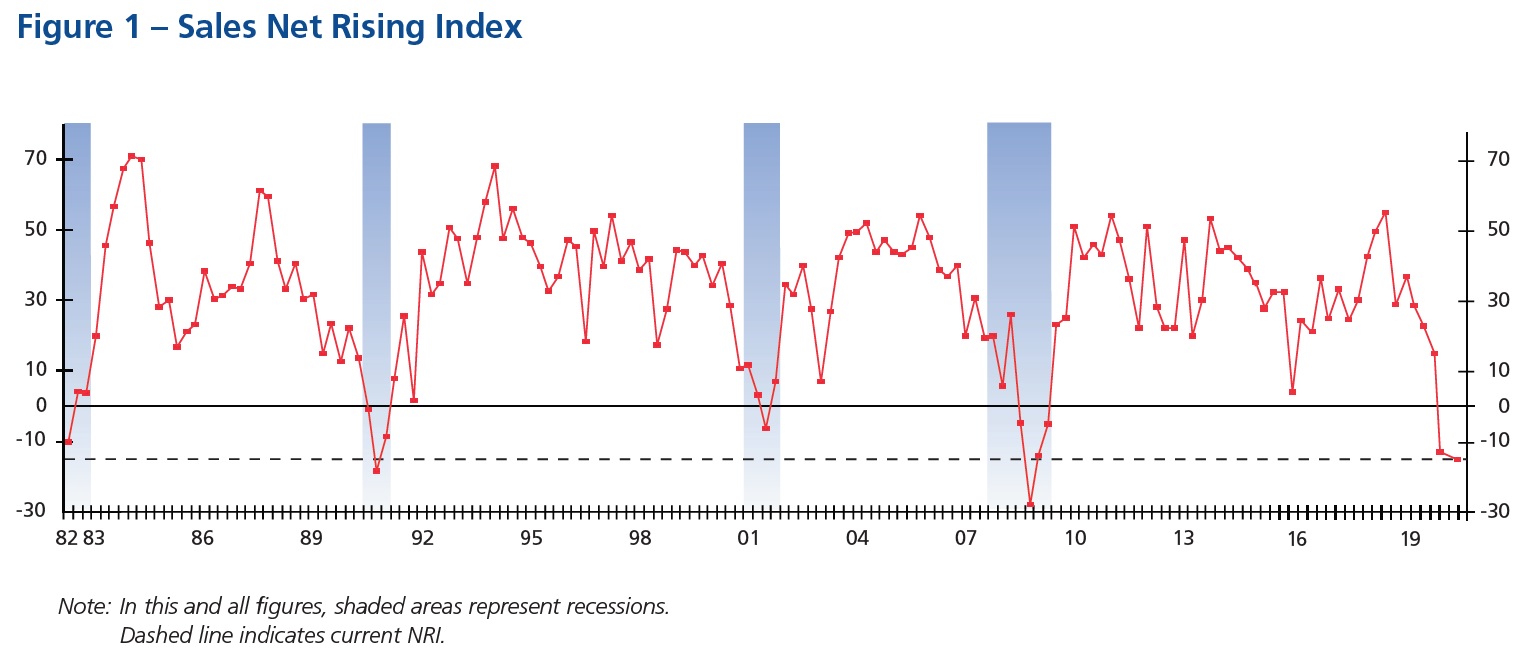

• The Net Rising Index (NRI) for sales—the percentage of panelists reporting rising sales minus the percentage reporting falling sales—remains generally unchanged, falling one point to -14 from -13 in April’s survey. While overall the NRI remains at the lowest level since 2009, the shifts by industry are dramatic. The forward-looking NRI for anticipated sales increases over the next three months rose significantly in July, from -55 in April to 18 in July.

• Profit margins improved slightly in Q2 2020, but are still at historically low levels. The NRI for profit margins rose 4 points to -25, the second-lowest reading since 2009. The forward-looking NRI for profit margins reversed most of April’s decline, increasing 50 points to a reading of 7 in July, with gains across all industry sectors. The dramatic swing was led by a 125-point improvement in the goods-producing industry.

• The NRI for prices charged is -15, the lowest NRI since 1987. Only 7% of respondents report that their firms had raised prices in the past three months, while 22% report falling prices.

• The NRI for materials costs dropped further into negative territory after a four-year streak in positive territory that ended in April. The NRI for expected costs snapped back to 1 from a reading of -21 in April.

• Hiring at respondents’ firms had, on net, stagnated for the previous two quarters, but the NRI fell to -19 in July, the lowest since 2009. The majority of respondents reports employment was unchanged in Q2 2020, but the share of firms experiencing rising employment diminished significantly from 19% in April to 5%. NRIs are negative across all sectors, with the goods-producing sector registering the most negative NRI of -55. The outlook for employment has improved significantly since April, with 22% of respondents anticipating employment increases at their firms compared with only 1% in April.

• The NRI for wages and salaries dropped into negative territory for the first time since 2009. Nearly a fifth of respondents indicates their firms reduced wages and salaries in Q2 2020, compared with zero respondents in the final quarter of last year. Looking ahead, 82% of respondents expect wages to stay the same, with the remainder equally balanced between expecting wage hikes and wage cuts.

• The shares of respondents reporting skilled and unskilled labor shortages shrank significantly from the April 2020 survey. The percentage reporting skilled labor shortages declined to 16% from 21%, and unskilled labor fell to 3% from 8%. The share of respondents reporting no shortages continued to rise in July to 64% from 52% in April.

• The NRI for capital spending fell further, from -4 in April to -19 in July. The NRIs for all sectors declined compared with those recorded in April. The forward-looking NRI for capital spending rose from -40 in April to 0 in July, but the majority of respondents expects no change in capital spending in the next three months.

• Firms primarily adopted three special measures to counter the financial impact of COVID-19 since March: imposing a hiring freeze (cited by 49% of panelists), terminating employees (34%), and furloughing employees (34%).

• Respondents’ near-term outlook stopped deteriorating in July relative to April’s survey. Fifty-four percent of respondents indicate their companies’ outlook is “About the Same,” compared with one month ago—a significant increase from 23% of respondents in April.

• Fifteen percent of respondents report sales exceed pre-crisis levels, including 25% of respondents from the finance, insurance, and real estate (FIRE) sector. The majority of respondents (62%) reports that their firms’ sales are between 76-100% of pre-crisis levels.

• Eighty-five percent of respondents indicate their firms can “stay afloat” for longer than 6 months without federal assistance, up from 74% in April. The transportation, utilities, information, and communications (TUIC) and FIRE sectors appear to be the most resilient, with 100% and 92% of respondents from those sectors, respectively, reporting they can last longer than 6 months.

• One in three respondents reports that their firms have already resumed normal operations. The FIRE sector has had the most firms resume normal operations (42%), followed by services sector firms (35%). Twenty-nine percent of respondents don’t expect to return to normal operations for more than six months, up significantly from 16% in April.

• The majority of respondents (74%) indicates that their firms have not applied or will not apply for Main Street Lending Program loans. Only 4% have applied for a loan or are considering it.

• Fifty-eight percent of respondents expect the national unemployment rate to be between 6.1% and 8% in June 2021. A quarter of respondents expects the unemployment rate to be greater than this range, while 17% expect it to be lower.

• Two out of three respondents “strongly agree “or “agree” that their firm’s experience with COVID-19 will lead to more flexible hiring and working arrangements at their firms in the future. More than 80% of respondents indicate their firms will have some degree of remote working for employees post-crisis.

• Government-ordered restrictions are impacting business operations of 56% of respondents’ firms. More respondents in the services and TUIC sectors than other industrial sectors report these restrictions are restricting their firm or its operations.

DOWNLOAD FULL SURVEY REPORT (Members only - sign-in required)